YN

Posts: 699

Status: offline

|

quote:

ORIGINAL: DesideriScuri

Isn't this, essentially, how the FDIC works? The "taxpayers" will fork over the funding to insure accounts up to 100k Euros, and the rest is "gone." Other than the $$ amounts, isn't that the FDIC?

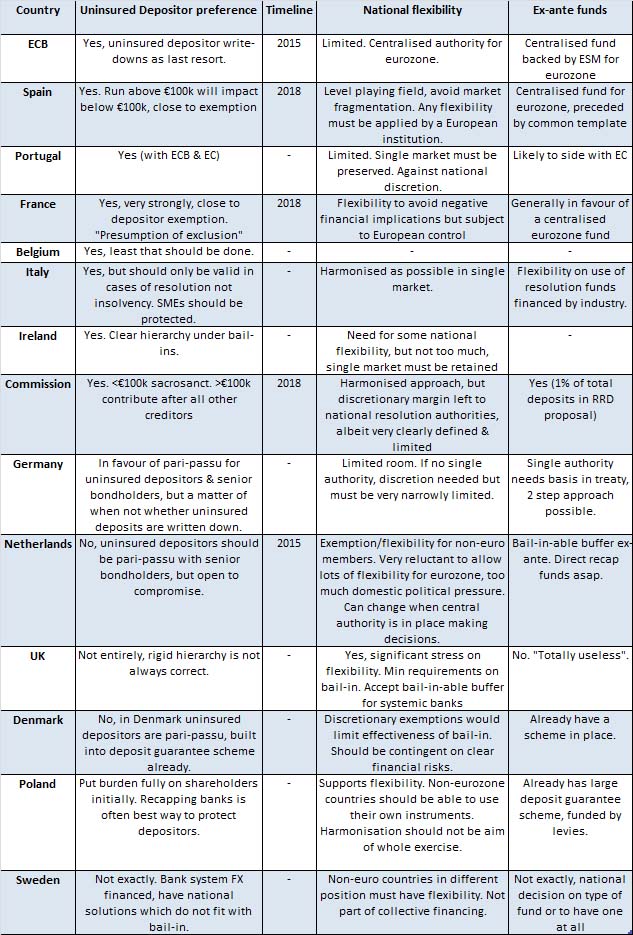

I wonder how many 100k+ Euros accounts there are now and how many get siphoned to be under 100k Euros in the first month after this ruling gets passed (assuming it gets passed).

Apparently that was not how your bank insurers (FDIC) worked in times past, and clawbacks of deposited money were not allowed.

However it is going to be in your future - The Bank Confiscation Scheme for US and UK Depositors

quote:

The 15-page FDIC-BOE document is called “Resolving Globally Active, Systemically Important, Financial Institutions.” It begins by explaining that the 2008 banking crisis has made it clear that some other way besides taxpayer bailouts is needed to maintain “financial stability.” Evidently anticipating that the next financial collapse will be on a grander scale than either the taxpayers or Congress is willing to underwrite, the authors state:

An efficient path for returning the sound operations of the G-SIFI to the private sector would be provided by exchanging or converting a sufficient amount of the unsecured debt from the original creditors of the failed company [meaning the depositors] into equity [or stock]. In the U.S., the new equity would become capital in one or more newly formed operating entities. In the U.K., the same approach could be used, or the equity could be used to recapitalize the failing financial company itself—thus, the highest layer of surviving bailed-in creditors would become the owners of the resolved firm. In either country, the new equity holders would take on the corresponding risk of being shareholders in a financial institution.

No exception is indicated for “insured deposits” in the U.S., meaning those under $250,000, the deposits we thought were protected by FDIC insurance. This can hardly be an oversight, since it is the FDIC that is issuing the directive. The FDIC is an insurance company funded by premiums paid by private banks. The directive is called a “resolution process,” defined elsewhere as a plan that “would be triggered in the event of the failure of an insurer . . . .” The only mention of “insured deposits” is in connection with existing UK legislation, which the FDIC-BOE directive goes on to say is inadequate, implying that it needs to be modified or overridden.

And apparently under your laws -

quote:

Now pay very careful attention, because part of the bankruptcy "reform" law in 2005 placed derivative claims in front of depositors in a business failure - including a bank failure.

What JP Morgan is claiming in the MF Global case is that the derivative trade (which is exactly what a "Repo to Maturity" trade is - it's a derivative) is entitled to preference in the case of MF Global over those who had cash there for safekeeping either as a margin deposit or just as free cash as you would hold free cash in a bank.

If a major bank blows up this very same claim, supported in existing Bankruptcy Law with the changes signed by George Bush in 2005, will be used to steal the entirety of your bank account, and if you detect the impending blowup shortly before it happens -- say, 90 days before -- you're still exposed to the risk through clawback!

I have often referenced how that "reform" law in 2005 was used to screw you blind as a consumer, all under the name of the "ownership society" and "responsibility." The truth is that this "reform" law was a raw example of financial******that was intended to and did assault you, the common consumer in America, for the explicit purpose of benefiting large financial institutions.

Don't run any crap about FDIC insurance in this sort of event either -- in the singular case of Bank of America we're talking about $77 trillion in face value of derivatives. While "notional" values are wildly beyond what anyone would have to pay (as that figure assumes the reference all goes to a literal value of zero) the fact remains that with even a 5% loss the amount of money required would be roughly equal to the entire US Federal Budget, which the FDIC clearly does not have -- nor could it acquire.

Let's Make The Clawback Risk REAL

So this is not the way things were done in the past.

|

Cyprus: The EU blueprint for bank failures? -

Cyprus: The EU blueprint for bank failures? -  Profile

Profile

New Messages

New Messages No New Messages

No New Messages Hot Topic w/ New Messages

Hot Topic w/ New Messages Hot Topic w/o New Messages

Hot Topic w/o New Messages Locked w/ New Messages

Locked w/ New Messages Locked w/o New Messages

Locked w/o New Messages Post New Thread

Post New Thread